How Organizations Respond to Fraud

You discover your erstwhile trusted employee has been skimming funds to support a gambling habit. What do you do?

Your first response is possibly unprintable, and understandably so. Your cooler head will prevail, and look at a small series of options for recovery, and maybe a dollop of justice. If there are losses, especially substantial losses, you will look at the circumstances of the fraudster carefully and evaluate the alleged crime for prosecution. You will look into the possibility of recovery and what the sources of recovery might be. The disruptive impact of being the victim of a crime might very well turn your thoughts away from revenge to the more practical goal of remediation.

The case studies analyzed in the 2018 Report to the Nations on Occupational Fraud and Abuse suggest a range of options organizations choose in the wake of a fraud. The Report, a study published every other year by the Association of Certified Fraud Examiners (ACFE), includes actions both through internal mechanisms and through external legal channels.

How are fraudsters punished?

It will come as no surprise that 65% of the fraudsters were simply terminated. 12% of organizations agreed to a settlement with the perpetrator and 11% of organizations say the perpetrator was no longer with the organization. What you might not expect is that 6% of organizations took no action and another 8% put the perpetrator on probation or suspension. The methodology of the study asks participant organizations about their biggest fraud case in the recent past, so a no action result suggests there are some very complicated circumstances below the surface. At the least, these widely disparate outcomes imply that organizations conduct an investigation of the fraud, and the evidence might point to a prudent course of action other than termination.

The perpetrator’s position in the company impacts their punishment.

The perpetrator’s role in the organization clearly modifies the organization’s response. An owner or executive is much less likely to be terminated (44% compared with 65% overall), and also much more likely to receive no punishment (12% compared with 6% overall). 72% of ordinary employees who committed a fraud were terminated.

Law enforcement is not always involved.

In the legal realm, uncertainty is increased by the fact that the alleged fraudster is innocent until proven guilty. The outcome of a civil action or criminal prosecution is not a given. Still, in 2018, 58% of frauds were referred to law enforcement and 23% resulted in a civil suit—the majority of these legal actions were resolved favorably to the victim.

Legal uncertainty abounds.

Yet the legal uncertainty is reflected in the fact that 12% of fraud cases are settled by agreement even before any legal action is taken (18% of owner/executive cases). In the group of civil cases, 27% are settled by agreement. And, fully 15% of civil cases result in a judgment for the alleged perpetrator.

The risks deter some organizations from taking legal action. 38% of these organizations cited bad publicity as the main reason, and other risks might also impose costs. Compounding the reasons to avoid legal action is the fact that in 53% of cases the victim recovered nothing, zero dollars. The more victims lose, the smaller the proportion they recover.

It is clear that organizations look at the cost-benefit value in deciding on what course of action to take in response to a fraud. Revenge may feel good, but it doesn’t serve the organizations’ interests.

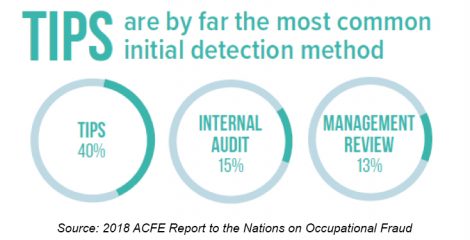

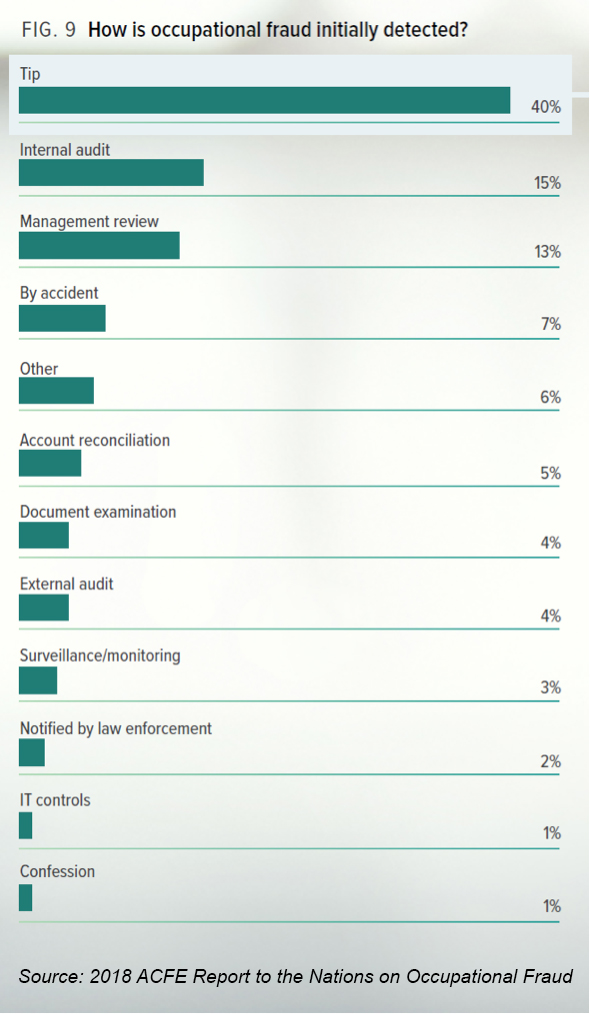

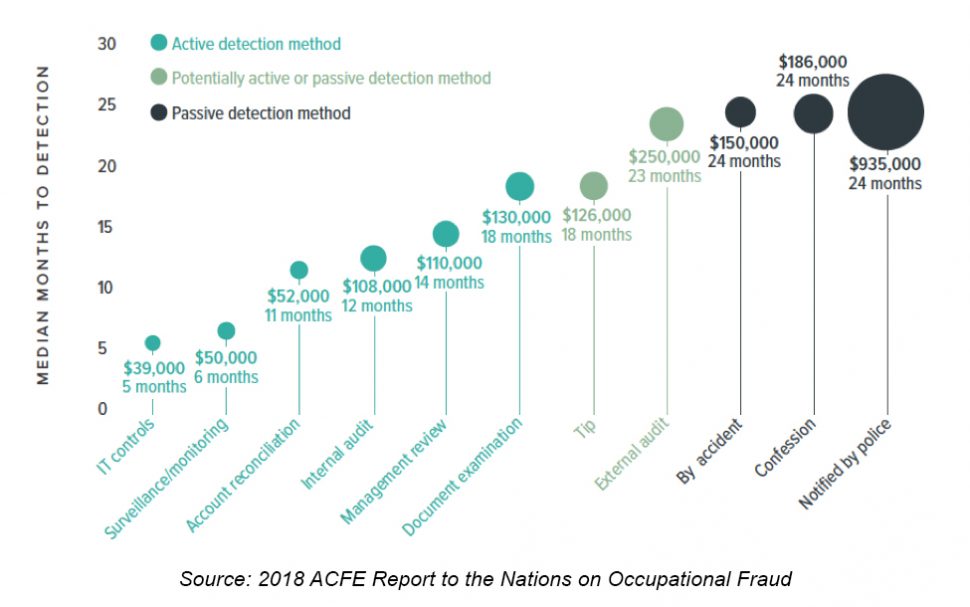

The point is clear, by choosing to proactively go after fraud, you put yourself in better standing to catch offenses early. This could be achieved by putting in place one of the six active detection methods. These proactive measures can be combined with other detection tools, such as hotlines. Hotlines and other reporting mechanisms were associated with a

The point is clear, by choosing to proactively go after fraud, you put yourself in better standing to catch offenses early. This could be achieved by putting in place one of the six active detection methods. These proactive measures can be combined with other detection tools, such as hotlines. Hotlines and other reporting mechanisms were associated with a