Fraud Week 2020: Cyberfraud and COVID-19

Think You’re Not at Risk? Think Again.

Our special 5-part Fraud Week Coffee Break Series continues today where we invite you to spend 10 minutes each day learning about various aspects of fraud detection and prevention through the eyes of our Certified Fraud Examiners and other fraud experts.

For this episode, we interviewed Steven Schwartz, Chief Revenue Officer for Periculus and a recognized innovation leader in the fields of risk management and cybersecurity. Periculus is a digital risk company specializing in helping small businesses measure, understand, and protect against digital risks so they can pursue growth. Before launching Periculus, Schwartz led strategy and insurance at Cytegic, one of the industry’s leading cyber risk quantification platforms, playing a vital role in the company’s successful acquisition by MasterCard in June 2020.

In its September 2020 Fraud in the Wake of COVID-19 Benchmarking Report, the Association of Certified Fraud Examiners (ACFE) reported, “Cyberfraud (e.g., business email compromise, hacking, ransomware, and malware) continues to be the most heightened risk for organizations, with 83% of respondents already observing an increase in these schemes and 90% anticipating a further increase over the next year.”

Many experts believe that organizations were simply unprepared from a cyber perspective for the pandemic and its resulting shift to a remote work environment where employees are now operating outside the usual infrastructure and oversight of their organizations.

As Schwartz explains, “We’re in an interesting time right now, where we’ve never been so polarized, yet so connected. With the increase in digital connectivity comes an exponential increase in the vulnerabilities and threats. The doors are open for attackers to exploit.”

Grab a cup of coffee and spend 7 minutes listening to Schwartz’s view on cyberfraud during COVID-19 and how organizations can better protect themselves moving forward.

How Can Organizations Better Protect Against Cyberfraud?

As with any type of risk an organization faces, it starts with an assessment to develop a true understanding of the risks you face and how those risks might impact your organization. From that place of understanding, you can make decisions about how to effectively mitigate or transfer those risks.

Schwartz explains it this way: “If you just tell me my risk is a 3 out of 5 and that’s all you tell me, I have no idea what that means to my business. But if you tell me I’m a 3 out of 5 with a financial impact of 2 million dollars, it becomes contextualized. And if we take that a step further and we’re able to demonstrate the controls you should invest in because they’re going to have the greatest impact in reducing your risk and financial impact and this is how much you should consider transferring via insurance, we can start to make sense of it all.”

We hope you enjoyed this Coffee Break episode. Come back tomorrow to hear from Neil Watson and lessons learned from real-life stories of fraud.

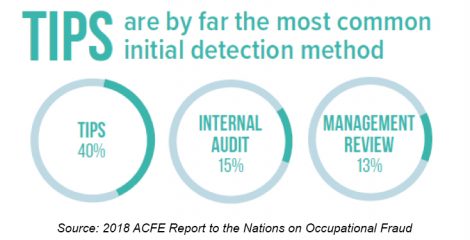

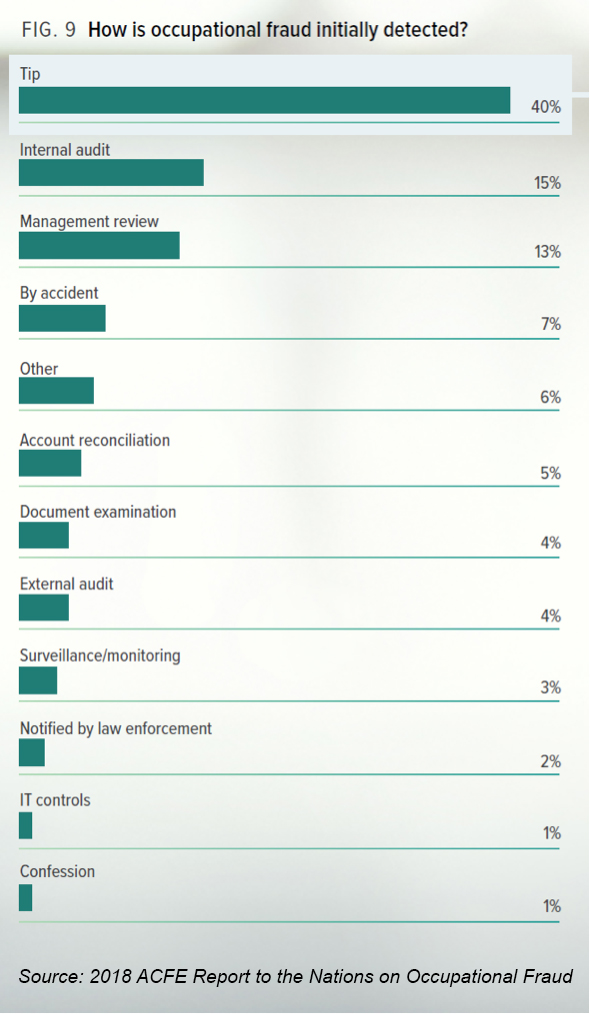

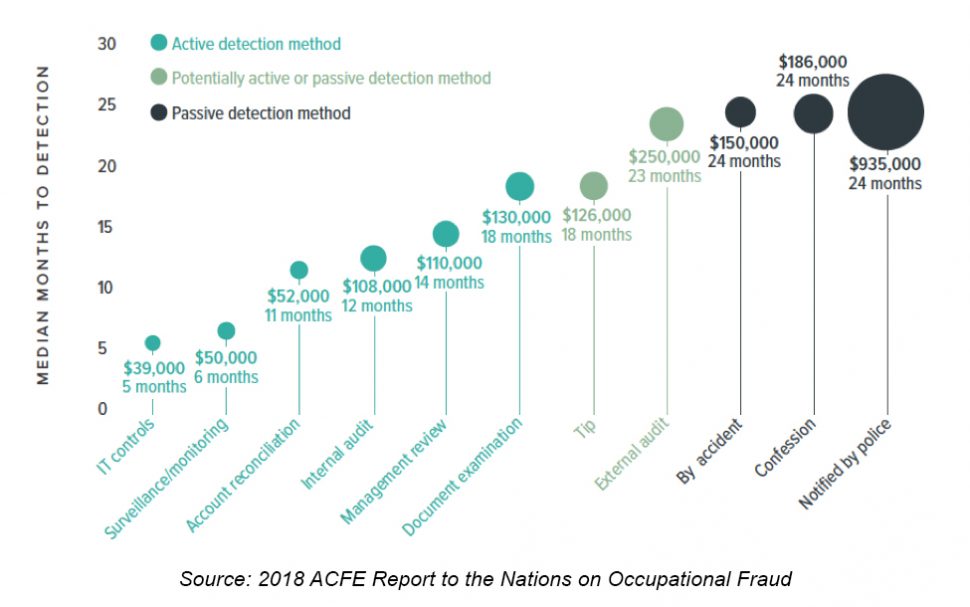

The point is clear, by choosing to proactively go after fraud, you put yourself in better standing to catch offenses early. This could be achieved by putting in place one of the six active detection methods. These proactive measures can be combined with other detection tools, such as hotlines. Hotlines and other reporting mechanisms were associated with a

The point is clear, by choosing to proactively go after fraud, you put yourself in better standing to catch offenses early. This could be achieved by putting in place one of the six active detection methods. These proactive measures can be combined with other detection tools, such as hotlines. Hotlines and other reporting mechanisms were associated with a